Supply chain financing in India has gained a lot of momentum. Recently, there have been government initiatives in this direction, most notably, introducing the e-invoicing system under the GST laws. The Indian market offers much potential for the growth of SCF; however, there are, as yet, many efforts to be made to capitalize on these opportunities.

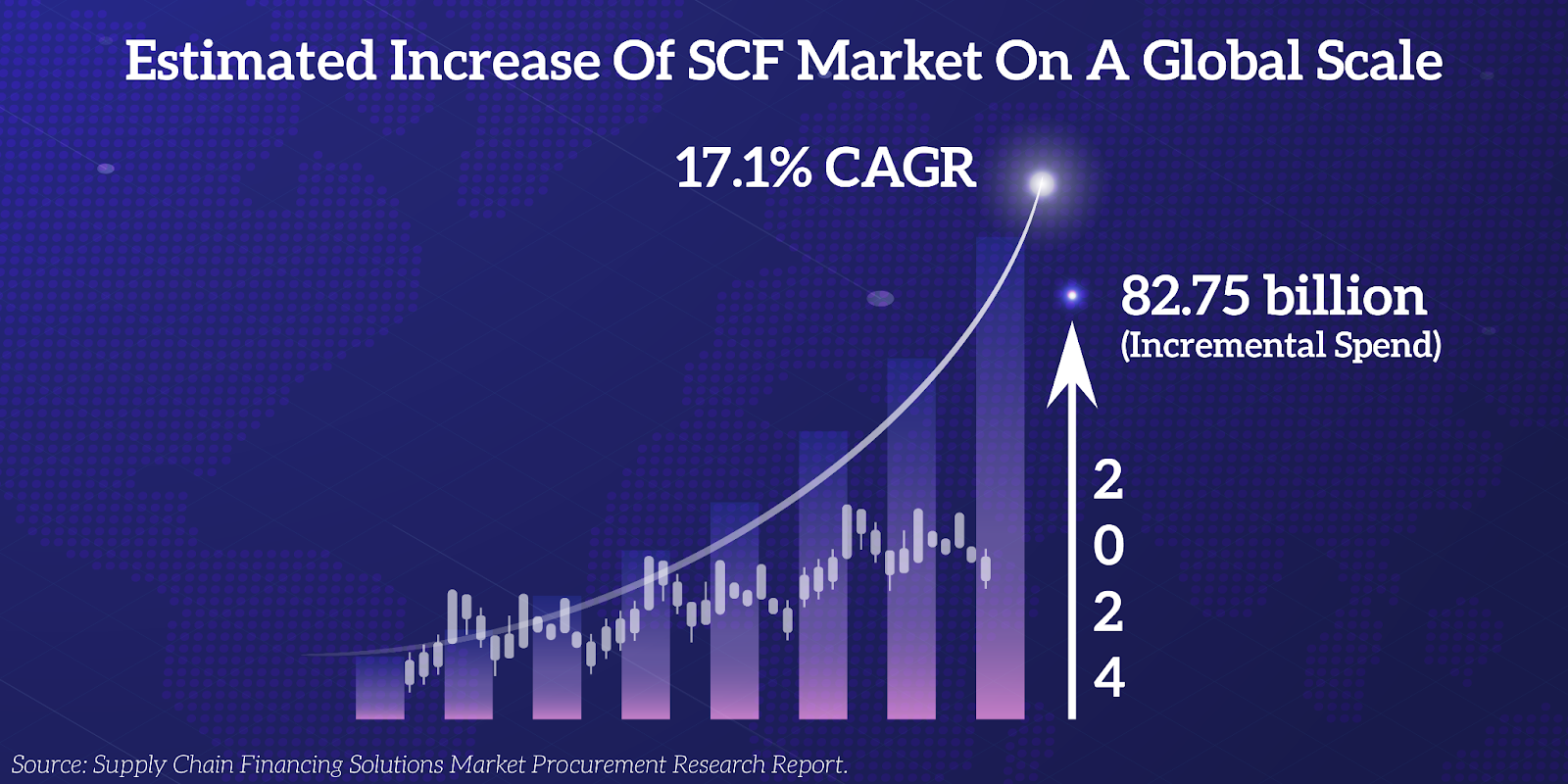

With a market size of approximately INR 60,000 crores [**Business Today], India’s booming supply chain finance business contributes to its economic prosperity. By streamlining the billing process, supply chain systems can connect all stakeholders, opening up a world of financiers and adding transparency. SCF ensures a win-win situation for the vendors, suppliers, anchors, and financiers.

4 essential things one should know about SCF

- It is not a loan but an extension of the buyer’s accounts payable and a shortening of the supplier’s accounts receivable.

- It ensures the availability and optimization of working capital.

- It is not just for large companies but also SMEs and firms with low credit ratings.

- These days, flexible SCF solutions provide multi-bank capabilities on a global scale.

Opportunities & Challenges for SCF in the Indian economy

Banks have an opportunity to fund various industries, which would help the corporation connect the entire supply chain – both upstream and downstream. Currently, PSU banks, private sector banks, MNC banks, and NBFCs make up most of the market.

The Challenges

- Banks must meet capital, liquidity, and regulatory criteria.

- Inadequate systems and infrastructure.

- Borrowers divert funds for other reasons.

- Lack of a unified platform for financiers.

- Onboarding and monitoring of dealers/suppliers are not simple.

The Opportunities

- With the Indian economy leaning towards e-commerce these days, there is an opening for banks to leverage this trend to support multiple supply chains.

- Banks have the opportunity to fund both forward and backward integration along the value chain with an integrated approach.

- Under-tapped markets in India such as commodities, consumer durables, electricals & electronics, FMCG, and agro-based industries have a great potential to fund their supply chains.

- New startups can use innovative templated products, creating opportunities for fintechs, banks, corporates, as well as the economy.

- Digital platforms and automation gives banks & stakeholders a big leg up in integration and information sharing. By implementing digital SCF platforms, firms can enable automation, workflow, risk mitigation, tracking, and monitoring of the end-to-end supply chain.

SCF: A source of optimism for Indian MSMEs

A vast majority (over 80%) of MSMEs in India cannot obtain standard bank credit and must rely on private funding sources at higher prices. Lenders are hesitant to lend to SMEs due to several issues, including a higher risk of default and a lack of standardized financial reporting. SCF assists lenders in overcoming these obstacles and extending finance to MSMEs.

India is home to over 63 million MSMEs according to the Ministry of Micro, Small, and Medium Enterprises, and MSMEs provide roughly 40% of India’s overall exports. Funding these MSMEs is a top priority among India’s economic objectives.

Thanks to SCF and technology, MSMEs can enjoy various benefits, including navigating working capital deficits and stabilizing operations. MSMEs can flourish with SCF.

Do SCF platforms play a significant role?

The answer is yes.

For financial institutions looking to capitalize on SCF programs, choosing SCF solutions that utilize the latest technology and have exquisite knowledge of how global programs of any size can function should not be an option but a priority.

Some key solutions that an ideal SCF platform would offer are:

- Stakeholder connectivity: Be it the buyer, supplier, or banker, an SCF software enables better transparency between all the critical stakeholders of the supply chain by connecting them through a single platform.

- Process automation: By leveraging technology to automate the workflow of tasks, documents, and information from end-to-end, banks can perform faster and collaborate smoothly across different departments.

- Globally scalable: Resilient platform that is not limited by varying geographies and can help firms big or small deal with different jurisdictions and different laws.

- Backend integration: Adapts quickly and efficiently to third-party and legacy systems used by traditional banks and financial institutions.

- Consolidated view: Provides a unified view of all the data and permits the buyers and sellers to self-serve by uploading and approving invoices and requesting finance when required.

- Real-time automation: Makes your job easier by automatically tracking and verifying documents in real-time, sending payment deadlines reminders, and monitoring the collection of outstanding balances.

- High-level security: Financial institutions and their clients require extraordinary security to protect confidential customer data and business information.

Firms new to supply chain financing and experienced players can confidently consider KAPPS SCF Plus, as it is a platform that offers the services mentioned above. Write to us to get customized SCF solutions for your financial service offerings.

Conclusion

Firms of all sizes require working capital to support their everyday expenses. Supply chain finance has evolved as a link between buyers and sellers, and it is expanding in new directions, enabling its adoption and expansion. Supply chain financing will become even more critical as the global economy continues to experience turmoil.